In our first working group on 15th October with panellists and attendees from over eighteen different countries, we opened up the floor to have an honest and open discussion about some of the most pressing problems facing the financial services industry and what needs to be done to bridge these gaps.

It was a truly eye-opening and insightful conversation, drawing on the experience and ideas from panellists across RegTech, Consulting, Banking, Insurance, Wealth and Asset Management providing us with real diversity of thought. Read on for an overview of the discussion.

The gaps are widening …

In the Bank of England seminar with Michael Sandel and Andy Haldane, they spoke about the increasing economic, social and political polarisation together with deepening income, wealth and technological inequality. These are incredibly pressing problems and Covid-19 seems to have revealed some key truths about their real magnitude which might have otherwise remained hidden for many more years.

How is the financial services industry a part of this problem and how can we tackle this?

Since the 2008 Financial Crisis, the financial services industry has come under increased scrutiny. The industry and regulators have taken steps to improve behaviours but there is still a way to go. Regulators have helped to facilitate cultural change but companies themselves must own this change if there is to be real, consistent impact.

We discussed the limitations of viewing success and making decisions through the narrow lens of short-term profitability and financial KPIs and how, although important, the fixation can cause companies to forgo the holistic viewpoint that inspires innovation and collaboration, generates good customer outcomes and creates fairness for all.

What does fairness really mean?

The lack of a unanimously agreed definition of fairness is a problem in itself. Perhaps the job of defining fairness is in one sense falling to individual members of society with their increasing ability to have their voices heard and consequently ‘vote with their money’. The latter posing a direct threat to long-term growth as ‘society will increasingly punish firms that do not get this right’ both with the power of their custom and who they choose to work for.

History has shown us many examples of stories on social media surrounding unethical business behaviour which have gone viral in a matter of hours, posing significant reputational risks to firms. Ignoring the societal change that is occurring and the increasingly powerful collective voice of individuals is not an effective long-term strategy.

So how can the industry generate long-term sustainable growth, attract future talent and contribute to a ‘fairer’ distribution of income and wealth?

Regulations and governance play an important role, but the volume and complexity of regulations has resulted in inefficient technical and operational processes. This is where it is important to consider the concept of culture change and the role of ‘purpose’ in shaping behaviours to create a ‘fairer’ financial services industry for all, however that may be defined.

Purpose could be a tool to unlock this long-term sustainable growth, bringing the industry closer to the needs of their consumers and clearer on the role which they are playing in the greater picture. As an example, the ICAEW’s paper ‘Culture And Purpose In Financial Services’, calls for a focus on purpose to prepare for the future in a sustainable way and prevent the industry from focusing solely on extracting value from their consumers.

Purpose can also help firms to reshape how success is defined and measured to enable the creation of profit in a sustainable way that society deems acceptable. Here at Change Gap, we established our business as a purpose-led company to ensure our actions align with our mission to help create a ‘stronger future for financial services’.

Speaking on the topic of purpose, our conversation moved onto how RegTech fits within this puzzle.

What are the barriers to RegTech adoption and how can we lower them?

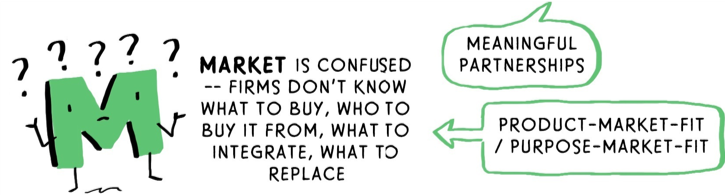

With seemingly never-ending waves of new regulations and different offerings from RegTechs, firms can find it difficult to know what to buy, who to buy it from, what to integrate and what to replace. Could the immaturity of the market be making things more complicated than it should be?

The point was raised that the real value is in making it simple for the client as compliance should not be overcomplicated. The objective should be to improve compliance rather than to adopt technology for the sake of technology.

One place to start is getting clear on the problems RegTechs are here to solve and the value that is being provided. This is achieved by ensuring product-market fit or ideally, purpose-market fit.

But how do we know if we are solving the right problem and ensure we are providing value to clients?

We highlighted the importance of domain expertise in tackling this problem and more specifically understanding the wider business, processes, people and regulatory requirements and how technology fits into this.

RegTechs being clearer on their product-market fit and their value proposition will help achieve maturity within the wider industry. This will also create space for healthy competition and collaboration between vendors, regulators and firms.

This led us onto our third and final topic surrounding the ecosystem and how healthy competition could work and benefit all parties.

Is it possible to generate a more sustainable, responsible and purpose-led ecosystem?

Having pointed out three main levers for achieving this including trust, partnership and healthy competition, our discussion focused on the importance of meaningful partnerships in driving long-term effectiveness.

But then arises the question of what that collaboration could look like?

The point was raised that the lack of a common language is impeding collaborations across the industry between regulators, firms and vendors. Progress in this area is critical in order to help firms to deliver on their purpose in a compliant manner.

In this though, we find a tension between the different roles of the regulator, both as an enforcer of rules and as a partner to collaborate with. Is there a balance that can be achieved? Public-private partnerships were noted as a key requirement for this.

The Bank of England transformation initiative around regulatory data reporting that Change Gap is participating in is a great example of inclusiveness helping to create a healthier ecosystem.

A further existing issue centres around firm culture, with existing indicators of success, internal policies and lack of commitment to change hampering RegTech implementations and stifling innovation and collaborative working.

Nonetheless, with open and transparent collaboration there is an opportunity to create a sustainable, responsible, thriving ecosystem but the specifics of how this can be achieved is a conversation that needs to be and will be continued in our future working group discussions.

What are your thoughts on our discussion?

If you want to be a part of the conversation, have your voice heard and help us in our mission to create a stronger future for financial services that is better for everyone, then please do reach out to us.

Our vision for the working group is to generate insights and achieve positive change through resulting collaborations. This vision is to bring positive benefit to those working in financial services as well as consumers of financial services and society as a whole.

Join us for our next discussion on 3rd December and let’s work together to make a real impact and drive positive change across the industry.